The Fire Protection System Pipes Market is witnessing a consistent upward trajectory, estimated at USD 23.7 billion in 2025 and projected to reach USD 42.9 billion by 2035, reflecting a 6.1% CAGR. This growth highlights a stable yet strong market dynamic, where rising fire safety regulations, urbanization, and modernization of existing infrastructure continue to drive global demand. While adoption has become widespread, the market remains far from saturation, creating a fertile environment for innovation and new entrants aiming to capture emerging opportunities in commercial, industrial, and residential sectors.

Regulatory Momentum and Modernization Fuel Market Growth

The continued global focus on fire safety is a key catalyst behind the expansion of the fire protection system pipes market. As governments enforce stricter building codes and safety standards, the demand for reliable fire protection infrastructure is escalating. These pipes play a crucial role in maintaining adequate water flow and pressure during fire emergencies, ensuring operational reliability and life safety compliance.

Insurance-driven mandates and liability considerations have intensified the demand for certified, high-quality piping systems that minimize risk exposure and enhance building safety. Developers and facility owners increasingly prefer materials that combine long-term performance, corrosion resistance, and easy installation, fostering a competitive edge for manufacturers investing in technology upgrades and innovative materials.

Steel Pipes Lead the Market as the Trusted Choice

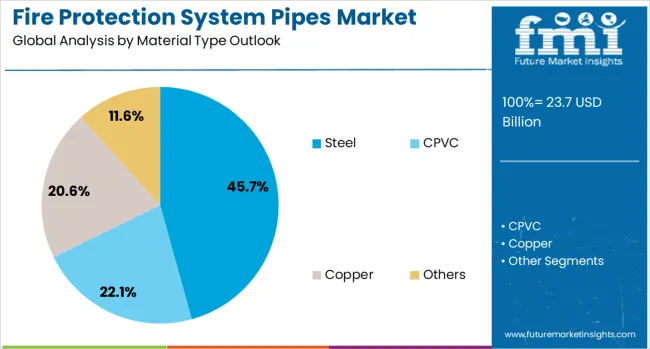

Among the material segments, steel pipes dominate with a 45.7% market share, reaffirming their status as the preferred material across commercial, industrial, and residential infrastructures. Their ability to withstand high pressure, temperature variations, and mechanical stress makes them indispensable for large-scale fire suppression systems.

Manufacturers such as Tata Steel, Victaulic, and Georg Fischer continue to advance steel pipe technologies, developing corrosion-resistant coatings and high-performance joints that meet stringent international safety codes. With building owners prioritizing reliability and compliance, steel’s proven durability cements its position as the backbone of fire protection infrastructure.

Commercial Sector Leads Demand with Growing Safety Investments

The commercial segment accounts for approximately 44.1% of total demand in 2025, supported by steady investments in office spaces, hospitality, healthcare, and retail facilities. Building managers are proactively upgrading systems to align with evolving safety standards and insurance protocols.

Retrofitting of existing properties has become a significant driver, with old systems being replaced by modern fire suppression networks designed for enhanced reliability and minimal maintenance. The combination of regulatory compliance and corporate responsibility is encouraging long-term partnerships between pipe manufacturers, fire protection system integrators, and commercial property developers.

Regional Insights: Asia Pacific at the Forefront of Growth

Regionally, the Asia Pacific market stands out as the most dynamic, led by China and India, which are expected to grow at 8.2% and 7.6% CAGR, respectively. China’s government mandates for advanced fire systems and extensive construction projects have created a robust domestic demand for certified pipes. Local and international manufacturers have ramped up production capacity, integrating smart coating technologies and CPVC solutions suited for high-rise developments.

India’s rapid industrialization and urban expansion also play a pivotal role. Domestic leaders like Tata Steel and Astral Pipes are innovating premium-quality, cost-effective fire protection solutions, supported by increasing construction in Tier 1 and Tier 2 cities.

In Europe, Germany (7.0% CAGR) and France (6.4% CAGR) remain critical markets, bolstered by strict safety codes, government mandates, and strong construction sectors. The United Kingdom, growing at 5.8%, continues to prioritize retrofitting programs across healthcare, education, and residential sectors, reinforcing the role of advanced fire protection technologies.

The United States exhibits stable growth at 5.2% CAGR, with strict NFPA and OSHA codes compelling both public and private sectors to modernize outdated systems. Meanwhile, Brazil’s 4.6% CAGR signals gradual but steady adoption as awareness of fire safety rises in urban centers.

Emerging Technologies and Smart Infrastructure Integration

A defining trend reshaping the market is the integration of smart and connected fire protection systems. IoT-enabled monitoring solutions are transforming traditional piping networks into intelligent systems capable of tracking flow rates, pressure levels, and potential leaks in real time. This digital integration supports predictive maintenance, enhances response times, and ensures compliance with modern building management systems.

Material innovation remains another critical growth factor. Manufacturers are adopting advanced coatings, composite blends, and corrosion-resistant metals to enhance longevity and reduce maintenance needs. Prefabricated piping systems are also gaining traction, offering faster installation and reduced project downtime — an essential benefit for large-scale commercial and industrial projects.

Competitive Landscape: Collaboration and Innovation Define Success

The fire protection system pipes market is characterized by strong competition among global leaders and regional specialists. Johnson Controls International plc, Victaulic Company, and Tyco Fire Products dominate the high-end segment with integrated solutions combining valves, sprinklers, and advanced piping systems. Their focus on certification, mechanical joining technologies, and preassembled systems reduces installation time while improving safety.

Tata Steel Limited and China Lesso Group Holdings Ltd. leverage their massive production capacities to serve large infrastructure projects worldwide. Tata Steel’s expertise in high-grade steel pipes complements China Lesso’s leadership in thermoplastic solutions, particularly across Asia Pacific markets.

Mid-sized players such as Georg Fischer AG, Aliaxis Group S.A., JM Eagle Inc., Astral Pipes, and Zurn Industries LLC differentiate through modular systems, lightweight designs, and cost efficiency. Georg Fischer and Aliaxis are pioneering flexible piping networks for complex installations, while Astral and JM Eagle continue to expand thermoplastic offerings that appeal to both residential and commercial markets.

The market’s fragmentation allows new entrants to compete through innovation, sustainable materials, and localized service. However, success depends heavily on certification, compliance with international fire safety standards, and the ability to deliver end-to-end solutions tailored to customer needs.

Purchase this Report for USD 5,000 Only | Get an Exclusive Discount Instantly! https://www.futuremarketinsights.com/checkout/26190

Everything You Need—within Your Budget. Request a Special Price Now! https://www.futuremarketinsights.com/reports/sample/rep-gb-26190

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube