The blended cement market is preparing for a period of steady yet impactful growth, with forecasts showing expansion from USD 78.9 billion in 2025 to USD 123.7 billion by 2035. This reflects a compound annual growth rate (CAGR) of 4.6%. Unlike some materials industries that show cyclical or seasonal fluctuations, blended cement demonstrates consistent upward progression. Between 2020 and 2025, values rose linearly from USD 63.0 billion to USD 78.9 billion. Looking ahead, projections suggest a smooth climb, surpassing USD 118.2 billion in 2034 before reaching USD 123.7 billion the following year.

This stability is not coincidental. Demand is being shaped by long-term drivers such as infrastructure development, urban housing initiatives, and industrial expansion, making blended cement a vital contributor to modern construction. Its adoption is being accelerated by sustainability imperatives and regulatory frameworks that encourage lower carbon emissions.

Why Blended Cement is Gaining Ground

The growing popularity of blended cement lies in its technical performance and environmental advantages. By incorporating supplementary cementitious materials (SCMs) like fly ash, slag, or calcined clay, blended cement reduces the reliance on clinker, a major contributor to carbon emissions in traditional cement production. This reduction in clinker factor not only lowers emissions but also enhances durability, long-term strength, and resistance against chemical attacks.

Governments and contractors are increasingly drawn to these benefits. Urbanization in emerging economies, infrastructure projects across Asia-Pacific, and renovation works in Europe and North America all depend on cement varieties that balance cost, performance, and sustainability. As contractors recognize the lifecycle cost savings and improved resilience of blended cement, adoption is accelerating across housing, commercial, and civil works projects.

Segmental Insights Highlight Market Potential

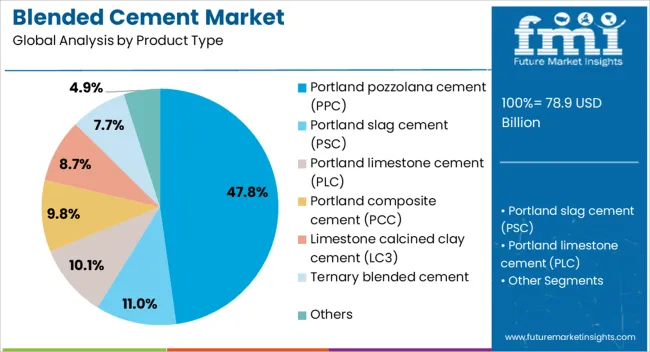

By product type, Portland pozzolana cement (PPC) stands as the leading segment, accounting for an estimated 47.8% share of revenues in 2025. Its superior durability, reduced heat of hydration, and cost efficiency make it ideal for large concrete structures where cracking risks must be minimized.

In terms of applications, the residential construction sector is expected to dominate with a 35% market share in 2025. Affordable housing programs, population growth, and government-backed initiatives are driving residential demand, with blended cement increasingly favored for its balance of quality and affordability.

On the SCM side, fly ash is set to command 37.2% of revenues in 2025, reflecting its role in improving workability, reducing permeability, and enhancing long-term strength. Its availability as a by-product of power generation provides both environmental and economic benefits, making it a sustainable cornerstone in cement production.

Regional Dynamics Shaping Global Growth

The global market is not moving in isolation—regional dynamics are shaping the pace and scale of growth.

China remains the frontrunner, projected to expand at a CAGR of 6.2%. Large-scale housing, transport infrastructure, and industrial facilities are fueling demand, alongside strong policy pushes to reduce clinker usage. Partnerships between domestic firms and global players are further strengthening supply chains.

India follows closely with a 5.8% CAGR, supported by urban housing programs, rapid infrastructure expansion, and abundant raw materials for blended varieties. Domestic producers are scaling up to capture rising demand while promoting durability and cost efficiency.

In Europe, Germany stands out with 5.3% growth, reflecting its emphasis on environmentally compliant materials and research-driven innovations in cement compositions. France and the UK also demonstrate healthy adoption, driven by public infrastructure projects and sustainability commitments.

The United States, though expanding at a more modest 3.9% CAGR, remains a valuable market. Infrastructure modernization, commercial construction, and renovation projects are sustaining steady demand for durable blended cement varieties like slag and fly ash blends.

Competitive Landscape: Established Giants and Emerging Innovators

The blended cement sector is marked by intense competition where established giants and emerging manufacturers alike are pushing boundaries in technology, production, and distribution.

Holcim has led the way through diversified formulations that optimize performance while cutting carbon intensity. Its expertise in combining fly ash, slag, and limestone with clinker ensures reliability for massive infrastructure projects.

Anhui Conch Cement Co., Ltd. dominates in China with vertically integrated operations, offering tailored blends suited to high-rise construction, transportation, and industrial projects.

Heidelberg Materials / HeidelbergCement has taken a different route, focusing on innovation in cement fineness and admixture compatibility, ensuring compliance with EU sustainability standards while maintaining durability.

Cemex S.A.B. de C.V. has expanded its global footprint with a portfolio of blends designed for diverse climates, providing rapid strength development and resilience.

In India, UltraTech Cement Limited and Ambuja / ACC leverage large-scale production networks and local distribution systems to meet demand for both residential and infrastructure projects, offering cost-effective yet high-performance solutions.

Regional players, too, are emerging with unique propositions—tailored formulations for niche projects, localized sourcing strategies, and competitive pricing that allows them to stand strong against global incumbents.

Opportunities for Stakeholders and New Entrants

The blended cement market is not just for established players. New manufacturers and stakeholders entering the space can capitalize on emerging opportunities. The rise of ternary systems, limestone-calcined clay concepts, and specialized grades for marine or transport projects opens avenues for innovation. Precast yards, retail bagged cement markets, and infrastructure-specific formulations provide entry points for smaller producers who can offer tailored, cost-efficient products.

Furthermore, as standards evolve and digitalization enhances plant efficiency, companies investing in advanced production technologies, admixture compatibility, and documentation processes will secure long-term contracts. Strategic collaborations between cement producers, admixture specialists, and testing laboratories will further smooth qualification hurdles and accelerate adoption.

Purchase this Report for USD 5,000 Only | Get an Exclusive Discount Instantly! https://www.futuremarketinsights.com/checkout/24709

Everything You Need—within Your Budget. Request a Special Price Now! https://www.futuremarketinsights.com/reports/sample/rep-gb-24709

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube