The machine glazed paper industry in Western Europe is gearing up for steady expansion over the next decade. Valued at USD 2.6 billion in 2025, the sector is expected to reach USD 3.5 billion by 2035, growing at a compound annual growth rate (CAGR) of 2.9%. This forecast reflects not only the strength of established players like Smurfit Kappa Group, International Paper Company, and Nippon Paper Industries, but also the determination of new entrants and regional manufacturers who are innovating to align with sustainability trends and modern consumer needs.

As industries such as packaging, hygiene, and printing continue to expand, machine glazed paper has emerged as a versatile and reliable choice. Its balance between functionality, cost-effectiveness, and environmental friendliness is setting the stage for a decade of transformation in Western Europe.

Driving Forces Behind Expansion

Several dynamics are shaping the industry’s positive trajectory. Rising demand from packaging sectors, particularly e-commerce and food delivery, has been instrumental in strengthening machine glazed paper adoption. With heightened awareness around sustainability, companies are under pressure to provide recyclable and biodegradable packaging solutions, and machine glazed paper has emerged as a natural fit.

Manufacturers are investing in energy-efficient technologies, optimizing production processes, and improving coating and finishing techniques to enhance product performance. This proactive approach allows established players and smaller firms alike to remain competitive in an increasingly regulated marketplace. Circular economy initiatives across Europe are further driving demand, reinforcing the role of machine glazed paper as an eco-friendly alternative to plastic packaging.

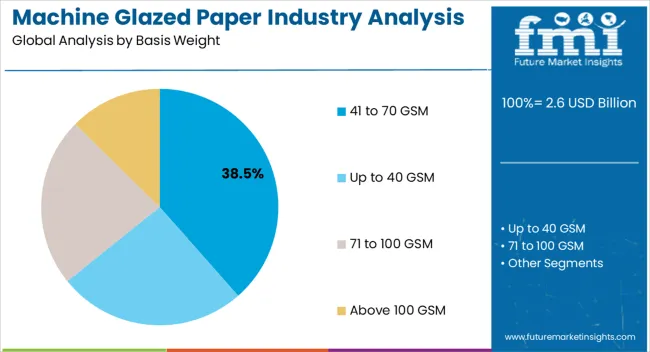

Segmental Insights Highlighting Market Potential

The industry’s structure reveals clear leaders across basis weight, paper type, and grade categories.

The 41 to 70 GSM basis weight segment, holding 38.5% of the market in 2025, represents the ideal balance of strength and flexibility. Its widespread application in both packaging and tissue underscores its continued dominance. Improved printability and smoothness have elevated its value across industries requiring both performance and compliance with food-contact safety standards.

On the paper type front, tissue paper remains at the forefront, with 55.2% of the share in 2025. High consumption in household and institutional hygiene applications ensures its leadership, strengthened by consumer demand for soft yet durable products. Innovations in creping and embossing techniques are enhancing tactile quality, making tissue products more appealing to consumers across Europe.

By grade, the unbleached segment leads with 60.4%, underlining the industry’s strong alignment with environmental priorities. Reduced chemical use, lower production costs, and its role in sustainable packaging make unbleached machine glazed paper an essential choice for manufacturers committed to eco-friendly practices.

Regional and Country-Level Growth

Growth across Western Europe is not uniform but reflects regional industrial strengths. The United Kingdom is expected to register a CAGR of 3.7% through 2035, demonstrating a robust appetite for sustainable packaging solutions in line with e-commerce growth and regulatory frameworks. Italy, with a projected CAGR of 3.4%, continues to showcase resilience and adaptability, reflecting evolving consumer behavior and its established paper production ecosystem.

These consistent growth rates in key European economies reinforce the wider regional trend of expanding adoption and diversification of machine glazed paper applications.

Key Opportunities Emerging for Stakeholders

For stakeholders, both established and new, opportunities are abundant. The rapid rise of e-commerce in Western Europe demands durable, printable, and recyclable packaging solutions—qualities that align perfectly with machine glazed paper. At the same time, innovations in barrier coatings and moisture resistance are opening pathways into specialized markets such as food, beverage, and pharmaceuticals.

Manufacturers adopting sustainable practices and integrating recycled content into production are positioned to secure long-term competitive advantages. Moreover, the push toward circular economy frameworks across Europe presents a unique window for stakeholders to align products with evolving regulatory and consumer expectations.

Investment Insights

The dominance of kraft paper, securing an 81.9% industrial share in 2025, demonstrates its versatility and strong presence across applications ranging from packaging to industrial use. At the same time, the unbleached category’s significant 69.5% share highlights an industrial inclination toward minimally processed, environmentally friendly paper products. Together, these trends shape the industrial narrative of Western Europe as manufacturers increasingly prioritize strength, durability, and sustainability.

Market Leaders and Rising Players

Prominent global players, including Smurfit Kappa Group, Mondi Group, Stora Enso, Billerud, and Heinzel Group, continue to set benchmarks in terms of production efficiency, scale, and innovation. Their sustained focus on quality improvement and energy-efficient processes enables them to remain at the forefront of the industry.

Simultaneously, smaller manufacturers and new entrants are embracing niche opportunities by innovating with specialty coatings, recycled materials, and customized grades of machine glazed paper. Their contribution to expanding the industrial landscape is equally vital, as they address unique regional demands and diversify the supply chain.

Notably, BillerudKorsnäs AB’s acquisition of Verso Corporation in March 2025 has reshaped the competitive dynamics. By adding expertise in coated groundwood and niche paper products, the acquisition strengthens Billerud’s foothold in Western Europe and signals a trend toward consolidation in the industry.

Future Outlook

Looking ahead, the machine glazed paper industry in Western Europe will continue to be shaped by sustainability imperatives, consumer preferences, and technological advancements. By 2035, the sector is expected to solidify its role as a cornerstone of the packaging, tissue, and printing industries, with rising investments ensuring innovation and compliance with evolving regulatory standards.

For stakeholders considering investments, the coming decade offers a mix of stability and innovation. Established players are enhancing capabilities, while new manufacturers entering the market have ample opportunity to carve out specialized niches by aligning with sustainability-driven demand. The result is a competitive yet collaborative ecosystem where both established and emerging firms stand to benefit.

Purchase this Report for USD 5,000 Only | Get an Exclusive Discount Instantly! https://www.futuremarketinsights.com/checkout/18685

Everything You Need—within Your Budget. Request a Special Price Now! https://www.futuremarketinsights.com/reports/sample/rep-gb-18685

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube