As diabetes continues to impact millions worldwide, the global non-invasive blood glucose monitoring devices market is poised for strong expansion. Valued at USD 9.3 billion in 2025, the market is projected to more than double, reaching USD 21.9 billion by 2035 at a steady CAGR of 8.9%. This growth reflects both a rising global demand for user-friendly solutions and the rapid evolution of breakthrough technologies that aim to make blood sugar monitoring painless, continuous, and more reliable.

Why Non-Invasive Monitoring is the Future

For decades, patients with diabetes have relied on finger-prick tests or invasive continuous glucose monitors, often facing pain, discomfort, and risks of infection. As adherence rates remain low with traditional methods, the healthcare industry has turned toward non-invasive alternatives. These devices utilize optical, electromagnetic, and spectroscopic technologies to measure glucose levels without puncturing the skin.

From wearable wristbands to advanced smartphone-linked sensors, the shift is being driven by patient demand for comfort, combined with clinical requirements for accuracy and real-time monitoring. With the global diabetes population rising, particularly in Asia and North America, the non-invasive approach is seen not only as a convenience but as a necessity for better disease management and prevention of complications.

Market Dynamics: Technology Meets Demand

The industry’s rise is fueled by significant advancements in sensor miniaturization, algorithm refinement, and wireless connectivity. Devices now allow seamless integration with smartphones and cloud platforms, offering patients trend analysis and physicians remote access to real-time data. Telemedicine adoption further strengthens this trend, making it easier for patients in both developed and emerging economies to stay connected with their healthcare providers.

Regulatory bodies are also showing increasing support for innovation in this space, encouraging research and approving pilot programs that bring these devices closer to mainstream adoption. Venture funding and strategic partnerships between medical device giants and technology companies are also accelerating development.

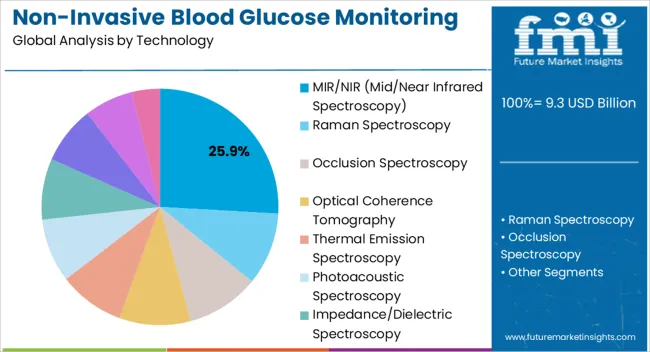

Insights into Leading Segments

The market is segmented by technology, modality, and end-user applications.

The MIR/NIR (Mid/Near Infrared Spectroscopy) segment is expected to lead with a 25.9% share in 2025, leveraging light absorption patterns to detect glucose levels painlessly. With continuous refinements in calibration algorithms, MIR/NIR technology is emerging as one of the most commercially viable solutions, particularly for wearable applications.

By modality, wearable devices dominate with 61.3% market share in 2025. Compact, lightweight, and lifestyle-friendly, wearables allow for discreet monitoring while providing real-time alerts for hypo- or hyperglycemia. Their compatibility with mobile ecosystems makes them a patient favorite and positions this segment as a key driver of future growth.

On the end-user side, hospitals account for 45.7% of market share in 2025, driven by adoption in inpatient and outpatient diabetes management. Hospitals not only deploy these systems to improve patient comfort but also act as validation grounds for new technologies, giving them credibility and driving broader clinical adoption.

Global Growth Outlook

Geographically, growth is not uniform but reflects distinct regional drivers:

- China is set to lead with a remarkable 12.0% CAGR, driven by a massive diabetes population, government investments, and strong domestic innovation.

- India, growing at 11.1% CAGR, is quickly becoming a hotspot for affordable, scalable glucose monitoring technologies that serve both urban and rural populations.

- Germany and France show strong growth within Europe, benefiting from robust healthcare infrastructure and early adoption of advanced diabetes technologies.

- The USA, valued at USD 3.2 billion in 2025, will reach USD 6.7 billion by 2035, growing at 7.6% CAGR, reflecting the country’s leadership in tech-enabled healthcare solutions.

- While Brazil records the lowest CAGR of 6.7%, it still signals a positive trajectory, underpinned by growing investments in public health initiatives.

Industry Leaders and Emerging Innovators

The competitive landscape includes established giants such as Abbott Laboratories, Dexcom Inc., Medtronic plc, and Senseonics Holdings, all of whom are expanding portfolios with non-invasive solutions to complement their invasive continuous glucose monitoring devices. These companies leverage global distribution channels and regulatory expertise to maintain their leadership.

Emerging innovators such as Nemaura Medical, DiaMonTech GmbH, OrSense Ltd., Know Labs Inc., and CNOGA Medical are making waves with proprietary technologies that challenge traditional players. Their agility and focus on specialized solutions make them attractive to both investors and strategic partners.

Meanwhile, tech-driven companies like Apple Inc. and Verily Life Sciences bring consumer electronics expertise into the medical arena, working on integrating glucose monitoring into multi-functional devices such as smartwatches. This cross-industry collaboration is expected to further reshape the competitive environment.

The Stakeholder Opportunity

For investors, stakeholders, and new manufacturers, this market presents multiple entry points. Established companies are pushing boundaries with large-scale R&D budgets and regulatory approvals, while start-ups are innovating with niche technologies and user-friendly designs.

Hospitals, research organizations, and healthcare providers also benefit from early adoption, as non-invasive monitoring promises better patient outcomes, reduced workloads for healthcare staff, and improved compliance. Governments and policymakers stand to gain from reduced long-term costs associated with diabetes complications by supporting widespread adoption of these devices.

Challenges on the Horizon

Despite optimism, challenges remain. High development costs, stringent regulatory requirements, and the need to balance accuracy with non-invasiveness are hurdles that manufacturers continue to face. Device calibration across diverse patient populations and ensuring affordability for developing regions are critical areas that require ongoing attention.

However, as algorithms improve, sensors evolve, and production scales, many of these barriers are expected to decline over the next decade, paving the way for mass adoption.

Purchase this Report for USD 5,000 Only | Get an Exclusive Discount Instantly! https://www.futuremarketinsights.com/checkout/2613

Everything You Need—within Your Budget. Request a Special Price Now! https://www.futuremarketinsights.com/reports/sample/rep-gb-2613

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube