The global biopolymer closure market is set to embark on a decade of rapid transformation as sustainability becomes the cornerstone of packaging innovation. Valued at USD 1.3 billion in 2025, the industry is forecast to double in size, reaching USD 2.6 billion by 2035. This strong growth trajectory, marked by a CAGR of 7.2%, is driven by international bans on petroleum-based plastics, a surge in eco-conscious consumer choices, and rising adoption across food, beverages, pharmaceuticals, and cosmetics.

The Rise of Biopolymer Closures

The momentum behind the biopolymer closure industry is no accident. Over the last decade, governments worldwide have intensified action against single-use plastics, forcing packaging manufacturers to rethink design and materials. Between 2020 and 2024, steady growth was recorded as polylactic acid (PLA) and starch-based blends became cost-effective, scalable alternatives to traditional plastics. Screw caps and flip-top closures gained traction in the beverages and pharmaceutical sectors, aligning with global recyclability and compostability targets.

By 2035, the shift will be undeniable. With biopolymer closures accounting for an ever-larger portion of packaging, the industry will serve as both a business opportunity and a moral imperative for brands prioritizing sustainability.

Key Drivers of Market Growth

Consumer awareness of environmental issues is at an all-time high. Major food and beverage companies are rebranding with greener identities, turning to recyclable and compostable closures as part of their broader ESG commitments. Pharmaceuticals and cosmetics are joining the movement, with closures playing a critical role in sustainable packaging for liquid medicines and premium personal care items.

Technological advancements are also propelling growth. PLA and bio-polyethylene (bio-PE) are becoming more durable, offering better shelf-life protection and compatibility with high-volume production. Hybrid blends are expanding capabilities by improving barrier properties against moisture and oxygen, which is critical for perishable goods.

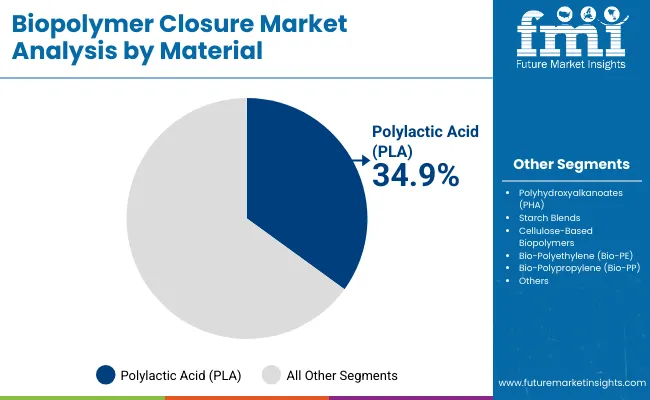

Segmental Highlights

When examining the market by material, PLA closures dominate with a projected 34.9% market share in 2025. Their affordability, biodegradability, and versatility make PLA the material of choice for bottles and jars, particularly in the food and beverage sector. By 2035, PLA will remain the most widely adopted biopolymer globally, supported by regulatory backing and consumer trust.

By closure type, screw closures will lead with 37.6% of the market in 2025. These closures are versatile, cost-effective, and easy to integrate into existing packaging lines. As e-commerce expands, the strength and reliability of screw closures will ensure they remain the preferred format for beverages, cosmetics, and pharmaceuticals.

In terms of application, bottles will anchor the market with 39.1% of the share in 2025. Single-serve beverages, liquid pharmaceuticals, and cosmetics are all heavily reliant on bottle packaging, reinforcing closures as a critical component.

Among end-use industries, food and beverages stand at the forefront with 42.4% of the share in 2025. High packaging volumes and strict environmental mandates have placed this segment at the heart of biopolymer closure adoption. With rising consumption of bottled water, dairy, and ready-to-drink beverages, the sector will continue to drive demand through 2035.

Regional and Country-Level Insights

Asia-Pacific is positioned as the epicenter of growth, with South Korea leading at a CAGR of 7.3%. Driven by strong government support for circular economy initiatives and rapid e-commerce adoption, South Korea is setting the tone for innovation in sustainable packaging. Japan follows closely at 7.2%, with premium cosmetics and beverages driving adoption.

China, with a projected CAGR of 6.7%, is boosting demand through packaging exports and fast-moving consumer goods (FMCG). India, at 6.6%, is harnessing plastic bans and rising bottled water consumption to fuel adoption of PLA-based closures.

In Western markets, the USA is expected to expand steadily at 6.8%, fueled by strong demand in beverages and pharmaceuticals. Germany and the UK, with CAGRs of 6.5% and 6.6% respectively, are seeing momentum from EU plastic bans and taxes that encourage recyclability.

Industry Leaders and New Entrants

The competitive landscape is moderately fragmented, with global leaders such as CJ Biomaterials, Beyond Plastic, Danimer Scientific, NatureWorks, FKuR, Green Dot Bioplastics, Natur-Tec (NTIC), ALPLA, Bericap, and AdvantaPure.

NatureWorks and Danimer Scientific are advancing PLA and PHA-based innovations, with partnerships such as Danimer’s collaboration with Bacardi to create PHA-based closures for premium spirits packaging. ALPLA and Bericap are focusing on integrating biopolymer closures into large-scale beverage packaging, while CJ Biomaterials emphasizes industrial scalability. Smaller firms like AdvantaPure and Beyond Plastic are targeting specialized niches in healthcare and cosmetics, proving that innovation is not limited to large corporations.

For new manufacturers looking to enter the space, opportunities abound in hybrid composites and recyclable closures tailored for e-commerce and household products. Stakeholders aiming to expand can focus on aligning cost-effective solutions with strict sustainability mandates.

Opportunities and Challenges Ahead

While the industry outlook is promising, challenges remain. The high costs of advanced biopolymers like PHA and bio-PP limit widespread penetration. Recycling infrastructure is uneven across regions, creating logistical hurdles for scaling adoption. Additionally, performance limitations, such as moisture resistance, remain barriers in certain applications.

However, the opportunities far outweigh these challenges. Healthcare, cosmetics, and premium consumer goods sectors are embracing biopolymer closures as a way to showcase sustainable branding. Integration of smart traceability features and automation compatibility is emerging as the next wave of growth, while partnerships between closure producers and FMCG giants continue to accelerate adoption worldwide.

Purchase this Report for USD 5,000 Only | Get an Exclusive Discount Instantly! https://www.futuremarketinsights.com/checkout/26741

Everything You Need—within Your Budget. Request a Special Price Now! https://www.futuremarketinsights.com/reports/sample/rep-gb-26741

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube