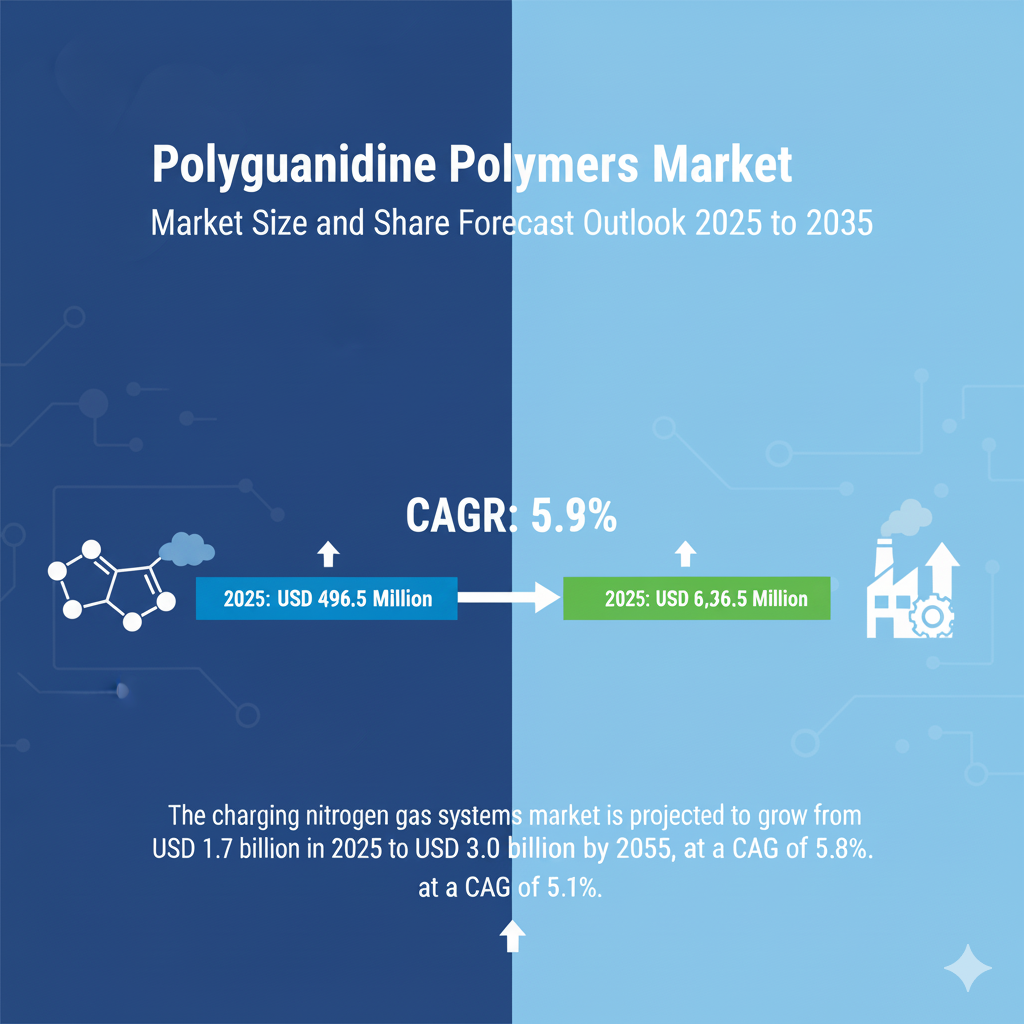

The global polyguanidine polymers market is on a steady upward trajectory, set to grow from USD 496.5 million in 2025 to USD 816.5 million by 2035. This translates into a total increase of USD 320 million over the decade, representing 64.5% growth at a compound annual growth rate (CAGR) of 5.1%. By the end of the forecast period, the market size will expand by nearly 1.64 times, supported by growing adoption of antimicrobial polymer technologies and increasing demand for specialty chemical solutions, particularly in water treatment and healthcare.

This rising demand highlights how essential polyguanidine polymers are becoming for industrial safety, clean water supply, and infection control in medical environments. For businesses, investors, and technology innovators, this market offers not only growth but also an opportunity to shape the future of antimicrobial solutions in industries worldwide.

The Growing Role of Polyguanidine Polymers

The market’s strength lies in its versatility. In 2025, water treatment alone will account for 45% of total demand, making it the leading application segment. From municipal water facilities to industrial plants, these polymers are critical in controlling microbial growth and ensuring safe water quality. Beyond water treatment, polyguanidine polymers are also carving out space in medical, personal care, and fabric treatment applications. The demand surge is fueled by heightened awareness of infection control and public health, coupled with stricter global standards for water safety.

Synthetic polymers dominate, accounting for 68% of the market share in 2025, thanks to their performance consistency, manufacturing scalability, and reliability across industries. With continued investment in advanced synthesis technologies, synthetic formulations are expected to remain the backbone of market growth.

Why the Market is Expanding

The primary growth driver is the rapid expansion of global water treatment infrastructure. As more cities and industries adopt advanced treatment facilities, the demand for antimicrobial solutions that can deliver consistent performance has intensified. Polyguanidine polymers provide long-lasting protection, ensuring microbial control even under complex operational conditions. Healthcare facilities also represent a rising demand source, with these polymers being adopted for infection control in medical products, coatings, and devices.

New environmental regulations are further pushing demand. As industries move away from conventional, toxic biocides, polyguanidine polymers offer an environmentally safer, non-toxic antimicrobial alternative. Manufacturers that can align product development with green chemistry principles are positioned to capture long-term market share.

Opportunity Pathways and Future Growth

By 2035, polyguanidine polymers are expected to unlock USD 120–150 million in incremental opportunities beyond baseline growth. These opportunities stem from multiple directions: optimizing synthetic polymer manufacturing, expanding into healthcare, tapping into emerging markets, and developing bio-based sustainable formulations. For instance, municipal and industrial water treatment continues to be a lucrative pathway, while advanced medical applications and antimicrobial consumer products represent premium, high-margin opportunities.

Emerging markets, particularly in Asia-Pacific and Latin America, are also poised to drive adoption. Industrialization, rising public health investments, and modernization of water treatment facilities in these regions present fertile ground for manufacturers that can offer competitive formulations and reliable technical support.

Established Leaders and Emerging Players

The competitive landscape of the polyguanidine polymers market reflects a balance between global chemical giants and specialized innovators. Established leaders such as SNF Floerger, BASF, Kemira, Evonik, Solvay, Dow Chemical, Ashland, Clariant, Huntsman, and Lubrizol are already setting high standards through their scale, technological innovation, and regulatory expertise. Their strength lies in robust R&D pipelines, advanced polymer synthesis capabilities, and global supply networks.

At the same time, a new wave of manufacturers—including Essential Polymers, Gellner Industrial, LG Chem, Kaneka, Osaka Organic Chemical, Lansen Chemicals, Sinofloc, and Maruzen Petrochemical—is bringing fresh energy to the market. These players are investing in niche antimicrobial technologies, green synthesis approaches, and customized solutions tailored for regional markets. Their agility and focus on specialized applications allow them to carve out significant opportunities despite competing with larger incumbents.

Together, both established stakeholders and new entrants are forming the technological backbone of this industry. Established firms bring credibility, regulatory alignment, and large-scale production, while newcomers introduce disruptive technologies and market expansion strategies.

Regional and Country-Level Growth

The polyguanidine polymers market demonstrates varied momentum across global regions. China leads with a forecast CAGR of 6.9% through 2035, supported by massive investments in water treatment infrastructure and specialty chemicals. India follows with 6.4%, propelled by rising water treatment needs and increasing industrial adoption of antimicrobial polymers. Germany, at 5.9%, showcases how advanced chemical industries are integrating innovative polymer technologies into established systems.

Brazil is expected to post 5.4% growth as it modernizes its water treatment infrastructure, while the United States will maintain steady momentum at 4.8%, leveraging its well-developed chemical industry. The United Kingdom and Japan will record 4.3% and 3.8% respectively, highlighting mature but innovation-driven markets. Collectively, these diverse regional growth patterns provide manufacturers multiple entry points depending on their scale, specialization, and strategic priorities.

Technology and Sustainability Trends

Advancements in polymer synthesis technology are reshaping the market, with manufacturers focusing on improved molecular design, enhanced antimicrobial effectiveness, and reduced environmental impact. Sustainable production practices, such as the integration of renewable feedstocks and green chemistry principles, are becoming industry benchmarks. Companies that successfully integrate performance optimization with environmental responsibility are likely to lead the market by 2035.

For many businesses, technical service and application support will also be a differentiator. Beyond product sales, long-term partnerships built through consulting, training, and performance optimization services are expected to create recurring revenue opportunities.

Purchase this Report for USD 5,000 Only | Get an Exclusive Discount Instantly! https://www.futuremarketinsights.com/checkout/26632

Everything You Need—within Your Budget. Request a Special Price Now! https://www.futuremarketinsights.com/reports/sample/rep-gb-26632

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube