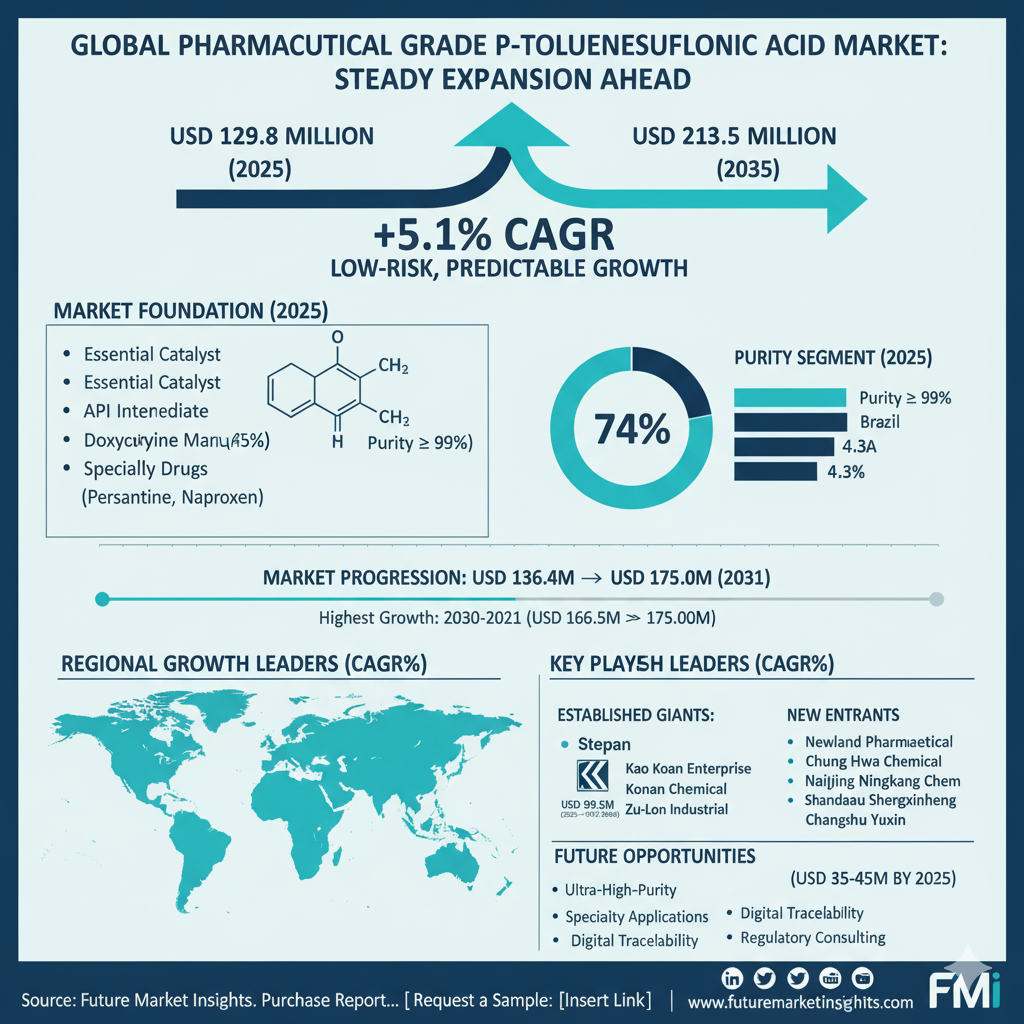

The pharmaceutical grade P-toluenesulfonic acid market is poised for a decade of steady expansion. Valued at USD 129.8 million in 2025, the market is forecast to reach USD 213.5 million by 2035, reflecting a compound annual growth rate (CAGR) of 5.1%. This trajectory illustrates not only consistent year-on-year growth but also a rare stability in an era where many chemical markets face volatility. From USD 136.4 million in 2026 to USD 175.0 million in 2031, the progression underscores a low-risk and predictable pathway for industry stakeholders.

A Foundation in Pharmaceutical Manufacturing

Pharmaceutical grade P-toluenesulfonic acid has long been recognized as an essential catalyst and intermediate in active pharmaceutical ingredient (API) production. Its role in synthesis processes such as doxycycline manufacturing, where it represents 45% of application share in 2025, highlights its indispensability. Beyond antibiotics, demand is rising in specialty drugs like persantine and naproxen, where complex synthesis protocols require ultra-pure intermediates to ensure efficacy, safety, and regulatory compliance.

The Purity≥99% segment dominates with 74% of market share in 2025. Its leadership is built on reliability, consistent performance, and alignment with regulatory expectations in advanced drug synthesis. For pharmaceutical manufacturers, this purity level represents both quality assurance and reduced risk, as deviations in chemical performance can compromise entire production lines.

Market Drivers and Steady Expansion

Growth is powered by the rising global demand for pharmaceuticals and increasing adoption of high-purity intermediates in drug synthesis. Expanding pharmaceutical facilities in Asia and Latin America, alongside modernization efforts in Europe and North America, create fertile ground for consistent demand.

Unlike volatile industries prone to raw material swings, the pharmaceutical grade P-toluenesulfonic acid market demonstrates narrow year-on-year growth variations between 4.8% and 5.4%. The highest growth occurs between 2030 and 2031, when values rise from USD 166.5 million to USD 175.0 million. The lowest, at 4.8%, comes in 2034–2035, when the market moves from USD 203.1 million to USD 213.5 million. Such predictability reinforces its role as a dependable sector for investment and long-term strategic planning.

Established Leaders and Expanding New Entrants

The competitive landscape features a balance between established leaders and ambitious new players. Stepan, Kao Koan Enterprise, Konan Chemical, and Zu-Lon Industrial anchor the market with decades of experience and deep regulatory expertise. Their ability to deliver high-purity intermediates with consistent documentation and global supply chain reliability cements their role as trusted suppliers.

Meanwhile, Newland Pharmaceutical, Chung Hwa Chemical, and Nanjing Ningkang Chem are broadening their portfolios, responding to pharmaceutical clients who demand not only quality but also value-added regulatory support and specialized formulations. Shandong Dongyue New Material Technology, Jiangsu Shengxinheng Chemical, Changshu Yuxin Chemical, and others are emerging as key regional manufacturers, enhancing their competitiveness with facility upgrades, quality certifications, and tailored solutions for regional pharmaceutical hubs.

This duality creates opportunities: established leaders safeguard reliability, while new entrants inject innovation, digital traceability, and cost-optimized models. For stakeholders, the combination promises both stability and advancement.

Opportunity Pathways for Growth

Beyond baseline expansion, incremental opportunities worth USD 35–45 million are opening by 2035. These include ultra-high-purity intermediates, specialty applications in complex drug synthesis, and digital supply chain traceability. Doxycycline remains the anchor, yet specialty drugs like persantine and oncology-focused formulations provide new growth avenues.

Emerging pharmaceutical hubs in China, India, and Brazil present fresh opportunities for suppliers to align with evolving regulatory standards and growing domestic manufacturing. Regulatory consulting, technical services, and premium packaging solutions are also emerging as differentiators, particularly for suppliers seeking long-term partnerships with global pharmaceutical giants.

Regional Growth Stories

China leads the market with a 6.9% CAGR, powered by its vast generic drug production base and government-backed pharmaceutical exports. With over 35% of Asia’s regional production capacity concentrated domestically, Chinese manufacturers are expanding facilities and upgrading standards to meet both local and international demand.

India follows at 6.4%, supported by its robust generic pharmaceutical exports and expanding active ingredient manufacturing. With rising collaborations between local producers and global firms, India is rapidly transitioning into a hub for high-purity intermediates.

Germany, with a 5.9% CAGR, exemplifies Europe’s focus on quality, innovation, and sustainable pharmaceutical synthesis. Here, P-toluenesulfonic acid plays a role in advanced specialty pharmaceuticals, supported by strong R&D and stringent EU regulations.

Brazil is advancing at 5.4%, aided by local capacity expansion and government initiatives to reduce import dependency. In North America, the United States grows steadily at 4.8%, driven by high regulatory standards, biopharmaceutical research, and oncology drug development. The United Kingdom and Japan, with growth rates of 4.3% and 3.8%, round out key contributors, reflecting the maturity of their pharmaceutical markets but maintaining a steady pull for advanced intermediates.

Innovation, Regulation, and the Decade Ahead

Advances in purification technologies and crystallization methods are driving consistency and performance improvements, while digital quality assurance platforms and traceability tools are beginning to reshape supply chains. These innovations position suppliers to better serve pharmaceutical companies that increasingly demand transparency, reliability, and compliance.

The integration of regulatory compliance features—such as batch certification, documented purity protocols, and enhanced quality control—will remain central to competitive positioning. Suppliers investing in regulatory services alongside chemical production will strengthen relationships with pharmaceutical companies seeking both reliability and reduced compliance risk.

Purchase this Report for USD 5,000 Only | Get an Exclusive Discount Instantly! https://www.futuremarketinsights.com/checkout/26639

Everything You Need—within Your Budget. Request a Special Price Now! https://www.futuremarketinsights.com/reports/sample/rep-gb-26639

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube