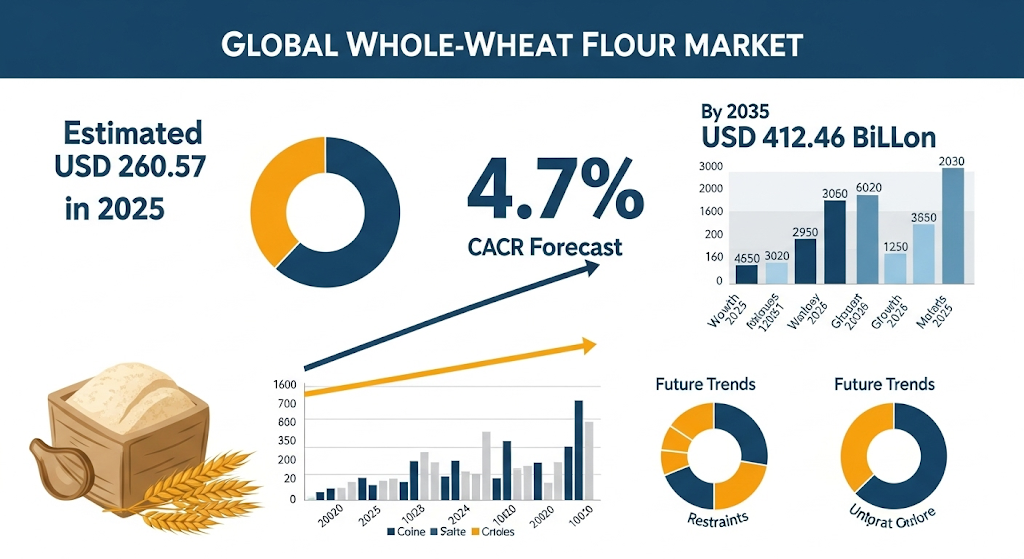

In an era where health meets sustainability, the global whole‑wheat flour market is approaching a watershed moment. As projected by Future Market Insights, the industry is expected to reach a market value of USD 260.57 billion in 2025, rising to USD 412.46 billion by 2035, with a compound annual growth rate (CAGR) of 4.7% (Future Market Insights).

This forecast underscores the grain’s rising importance in global diets—but behind the big numbers lies a more complex question: are consumers truly ready to embrace whole‑wheat flour at scale?

Gain Valuable Market Knowledge: Request a Sample Report: https://www.futuremarketinsights.com/reports/sample/rep-gb-9617

Health on a Plate, but at What Cost?

Whole‑wheat flour boasts a dense nutritional profile—fiber-rich and packed with essential minerals—making it a compelling alternative to refined flour. And yet, despite its rising reputation, actual consumption patterns remain sluggish in many developed countries. The problem isn’t awareness. It’s accessibility.

Whole‑wheat flour often costs more, has a shorter shelf life, and can yield denser textures in baked goods—an issue for consumers who prioritize price, convenience, and taste. Until these barriers are addressed, its potential risks remaining locked in premium aisles and niche markets.

Surge in Market Demand: Explore Comprehensive Trends and Analysis in Our Full Report: https://www.futuremarketinsights.com/reports/whole-wheat-flour-market

Global Momentum, Uneven Adoption

The projected market expansion reflects growing demand in Asia-Pacific and parts of Europe, where consumer preferences are shifting toward whole grains. However, in many Western countries, especially the United States, adoption is inconsistent. Institutional support, such as school programs or health-based food subsidies, remains weak.

Brands are innovating—introducing new blends, refining textures, and experimenting with sustainable sourcing—but the average shopper still sees whole‑wheat as an optional upgrade, not a baseline staple.

Innovation Is Not Enough Without Incentive

It’s not just about better products. The supply chain—from wheat growers to processors to retailers—must adapt. Whole-wheat flour requires more careful storage, and the grain’s outer layers (where nutrients live) are more susceptible to spoilage. That raises logistical costs and discourages widespread use unless incentivized.

Moreover, the economic logic needs to flip. When a healthier product is more expensive, adoption remains a luxury, not a lifestyle.

Will the Growth Stick?

The optimism in the FMI forecast—$260 billion to $412 billion in a decade—is a vote of confidence in consumer shifts and market evolution. But as any seasoned observer of the food industry knows, forecasts are not guarantees.

For the market to fulfill this potential, three things must happen:

- Price Competitiveness – Cost parity with refined flour must become a reality.

- Consumer Education – Awareness must turn into behavior change.

- Policy Support – Government and public institutions need to step up—through labeling, procurement standards, or incentives.

Final Take

Whole-wheat flour is no longer a fringe ingredient—it’s becoming a frontline player in the global conversation about food, health, and sustainability. But projections alone don’t move markets. People do. The $412 billion question is whether consumers—and the systems that serve them—are ready to make whole-wheat the new normal.

Leading Manufacturers

- The King Arthur Flour Company

- Gold Medal

- Bob’s Red Mill Natural Foods

- Stone Ground

- Georgia Organics

- Heartland Mill Inc

- Wheat Montana Anson Mills

- Siemer Milling Company

- Hodgson Mills

- Lindsey Mills

- Ardent Mills

- General Mills

- Conagra Mills

- Wiking Rogers Mills

- Kishan Exports

- Sunrise Flour Mill

- Belize Inc.

- Natural Way Mills

Explore Convenience Food Industry Analysis: https://www.futuremarketinsights.com/industry-analysis/convinience-food

Explore Convenience Food Industry Analysis: https://www.futuremarketinsights.com/industry-analysis/convinience-food

Key Segments of the Report

By Product Type:

By product type industry has been categorized into Bread Flour, Pancake Flour, Cracker Flour & Pizza Flour.

By Nature:

By nature, industry has been categorized into conventional & organic.

By Application:

By application industry has been categorized into Bread, Bakery Products, Biscuits, Rolls, Cookies, Buns, Sweet Goods, Desserts & Tortillas.

By Packaging:

By packaging format industry has been categorized into Supersacks, Bags & Bulk Tankers.

By sales channel:

By sales channel format industry has been categorized into B2B/Direct Sales, B2C/Indirect Sales, Hypermarket/ Supermarket, Retail Stores, General Grocery Stores, Specialty Stores & Online Stores.

By Region:

Industry analysis has been carried out in key countries of North America, Latin America, Europe, Middle East and Africa and Asia.