Local grocery store’s dairy aisle looks radically different than it did a decade ago. It’s a riot of colors and textures, dominated by tubs promising creamy indulgence without a single drop of cow’s milk.

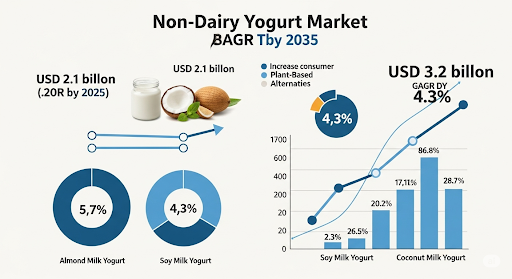

The isn’t just growing; it’s exploding, poised to expand from USD 2.1 billion in 2025 to USD 3.2 billion by 2035, expanding at a CAGR of 4.3%. This isn’t merely a trend; it’s a seismic shift, driven by an eager public seeking health, sustainability, and ethical consumption. But as a journalist who’s seen countless food fads rise and fall

I have to ask: beyond the virtuous veneer, what are we really buying into? Is this boom truly benevolent, or just another masterclass in marketing? This is more than just a market trend; it’s a critical moment for food transparency.

Unveil Market Trends: Get Your Sample Report Now:https://www.futuremarketinsights.com/reports/sample/rep-gb-4120

The Relentless March of Plant-Based Promise

The numbers tell an undeniable story of expansion. A compound annual growth rate (CAGR) of 4.3% through 2035 is not just impressive; it’s a roaring success. This isn’t some niche product anymore. It’s mainstream. Consumers, increasingly health-conscious, are flocking to non-dairy options for perceived benefits. Lactose intolerance is a major driver, especially in regions like Asia-Pacific, which Future Market Insights identifies as having explosive growth potential. While the United States stands out as the largest and most established market, India and China are poised to be the fastest-growing countries, each forecasted to grow at a CAGR of 5.1% over the same period, driven by a combination of high lactose intolerance rates, growing middle-class populations, and increasing health consciousness. This global push underscores the universal appeal manufacturers are tapping into.

Manufacturers are certainly capitalizing. We’re seeing an explosion of innovation: new flavors, protein-enriched varieties, low-sugar formulations, and a relentless focus on organic and “clean label” ingredients. Coconut, almond, oat, and soy bases are all vying for supremacy. This variety is exciting, no doubt. It offers genuine alternatives for those who can’t or choose not to consume dairy. The market is responding to a real demand, and innovation is clearly at its heart.

Rising Interest in Market Trends: Our Detailed Report Provides Essential Insights: https://www.futuremarketinsights.com/reports/non-dairy-yogurt-market

The Murky Waters of “Health” Claims

Yet, the rosy picture quickly becomes complicated when we peel back the layers of marketing. Non-dairy yogurts are often presented as universally “healthier.” But are they? It’s far from a simple yes. While they can be lactose-free and address specific dietary needs, achieving that familiar creamy, spoonable consistency without dairy’s natural structure can be a challenge. Manufacturers often rely on gums, starches, and other additives to mimic dairy’s mouthfeel. While generally recognized as safe, these ingredients might raise eyebrows for those truly committed to a “clean” and minimally processed diet. The very act of making a non-dairy yogurt look and feel like its dairy equivalent often requires significant industrial intervention. So, is it truly “clean,” or just cleverly engineered? This is a question the industry rarely addresses head-on.

The “Sustainable” Illusion: A Deeper Look

Then there’s the environmental halo. Non-dairy products are widely celebrated as the sustainable choice, a crucial step in mitigating the climate impact of traditional dairy farming. But this isn’t a blanket truth, and it certainly isn’t a simple equation. The supply chains for these “natural” ingredients are often vast, complex, and opaque. While the plant-based narrative is compelling, the sheer scale of the projected market growth demands a deeper inquiry into the actual environmental impact of cultivating these vast quantities of plant-based ingredients. “Increased focus on sustainability and ethical sourcing” is an “emerging trend,” which indicates it’s a developing area, not necessarily a universally ingrained practice throughout the rapidly expanding market. This leaves room for significant scrutiny.

Beyond the Buzzwords: A Call for Genuine Accountability

The non-dairy yogurt market is undeniably a commercial juggernaut. Its growth is propelled by powerful consumer desires for health, ethics, and environmental responsibility. But as profits soar towards that $3.2 billion mark, it’s incumbent upon the industry to move beyond surface-level marketing. “Clean label” must mean truly transparent ingredient sourcing and minimal processing, not just clever ingredient swaps. “Sustainable” must encompass the entire supply chain, from cultivation practices to manufacturing energy use, not just a favorable comparison to dairy. Consumers are increasingly sophisticated; they are looking beyond the pretty packaging. They want to know the whole story. If the non-dairy yogurt market is to truly live up to its perceived benevolence, it must embrace genuine accountability. Anything less is a disservice to the consumer, and to the planet. Demand more than just a buzzword; demand substance.

Key Company Profile

- General Mills, Inc.

- The Hain Celestial Group Inc.

- Danone SA

- Nestlé SA

- Chobani, LLC

- Forager Project, LLC

- Valio Ltd.

- Stonyfield Farm Inc.

- Daiya Foods Inc.

- Springfield Creamery Inc.

- Others

Explore Dairy and Dairy Products Industry Analysis: https://www.futuremarketinsights.com/industry-analysis/dairy-and-dairy-products

Key Segmentation

By Source:

As per Source, the industry has been categorized into Soy, Almond, Coconut, Oat, Rice, Pea, and Others.

By Nature Type:

This segment is further categorized into Organic, and Conventional.

By Sales Channel:

This segment is further categorized into HoReCa, Cafés, Bakeries & Patisseries, Hypermarket / Supermarkets, Convenience Stores, Wholesale Stores, and Online Retail.

By Flavor:

This segment is further categorized into Flavored and Unflavored.

By Form:

This segment is further categorized into Drinkable and Spoon able.

By Region:

Industry analysis has been carried out in key countries of North America, Latin America, Western Europe, Eastern Europe, Balkans & Baltic, Russia & Belarus, Central Asia, East Asia, South Asia & Pacific, and the Middle East & Africa.