Chickpea flour is no longer a niche pantry item. It’s booming—globally, unmistakably, and with huge implications for how the world eats. But as the flour racks fill with protein-rich powders claiming health and sustainability, we have to ask: are we just chasing another “clean” label trend, or finally waking up to an ingredient that actually delivers?

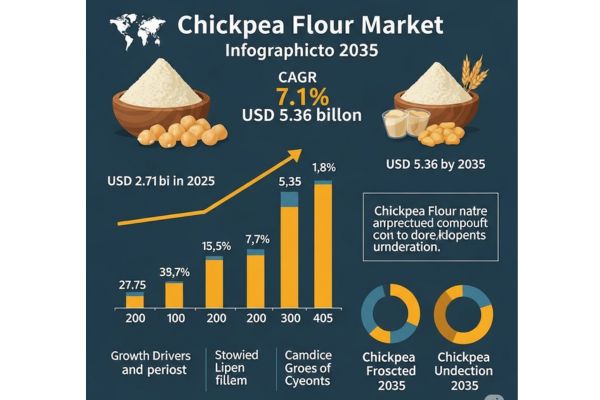

The market signals say it’s more than a trend. According to Future Market Insights (FMI), the chickpea flour market is expected to grow from USD 2.6 billion in 2024 to over USD 4.7 billion by 2030. That kind of growth doesn’t happen by accident. It’s the result of three converging forces: plant-based eating, gluten-free demand, and the global push toward nutrient-dense alternatives.

Still, the story isn’t all rosy. If anything, we’re in the middle of a moment where consumer interest is outpacing food policy, labeling standards, and nutritional understanding. The stakes? Health, trust, and a market ripe for misinformation.

Unveil Market Trends: Get Your Sample Report Now: https://www.futuremarketinsights.com/reports/sample/rep-gb-6126

A Protein Powerhouse or Another Wellness Gimmick?

There’s no denying the numbers. FMI projects the chickpea flour market to register a compound annual growth rate (CAGR) of over 6% between 2024 and 2030. Demand is particularly strong in North America, where consumers are increasingly seeking plant-based protein alternatives—and are willing to pay a premium for them.

But while chickpea flour is undoubtedly rich in protein and fiber, its commercial appeal often masks a lack of understanding. What matters is how the ingredient is processed, how it functions in food applications, and how consumers use it. Not every “chickpea flour” is created equal, and the current labeling environment makes it nearly impossible to distinguish between quality and filler.

Rising Interest in Market Trends: Our Detailed Report Provides Essential Insights: https://www.futuremarketinsights.com/reports/chickpea-flour-market

Global Appetite, Local Blind Spots

FMI’s data shows that Asia Pacific and Europe are driving significant demand, particularly due to established culinary uses and growing middle-class dietary shifts. Yet even as the global market matures, the United States continues to operate with a loosely defined set of food-labeling standards that barely reflect modern nutritional science.

That’s a problem. Because when demand grows faster than regulation, opportunism always follows. Without standards around processing, protein content, or glycemic response, “chickpea flour” becomes another vague claim. And consumers—especially those with food allergies or dietary conditions—are left guessing.

Health Food or Hazard?

As chickpea flour gets baked into everything from pasta to pastries, it’s being marketed as a “clean,” plant-based solution for just about every diet under the sun. But as with any ingredient enjoying a moment in the spotlight, the truth is more complex.

FMI’s report emphasizes its role in functional food innovation: egg replacements, gluten-free binding agents, and low-GI formulations. This isn’t fluff—chickpea flour is technically impressive. But that doesn’t mean it’s risk-free. Improper processing can leave anti-nutrients intact. Digestive issues, especially among new users, are not uncommon. Yet few brands explain how their flour is prepared, milled, or tested. They’re selling a story, not a science.

What the Industry Won’t Say

The most striking part of this market’s growth is how quietly it’s being framed. We’re not seeing public conversations around regulation, sourcing, or consumer literacy. Brands are racing to meet demand—but with little regard for what happens after the sale.

There is no unified guidance for foodservice providers using chickpea flour in bulk. There’s no consumer education campaign warning about potential digestive sensitivity. And there’s no national standard for what counts as “high protein” when it comes to legume-based flours.

That silence speaks volumes.

The Bottom Line

Chickpea flour deserves its moment—but not if it’s based on overpromising and under-informing. The market, as FMI shows, is clearly ready. But readiness isn’t just about revenue projections. It’s about whether consumers know what they’re really buying—and whether the industry is willing to tell them.

If we let the hype grow unchecked, chickpea flour could go the way of other once-revolutionary ingredients: misunderstood, misused, and eventually mistrusted.

But if we take this moment to demand transparency, invest in education, and push for regulatory clarity, this could be something else entirely. A rare case of food innovation that lives up to its promise.

Key Players Profiled in the Chickpea Flour Market Report

- Parakh Agro Industries Ltd

- Ingredion Incorporated

- Anchor Ingredients

- CanMar Grain Products

- The Scoular Company

- SunOpta

- Bean Growers Australia

- EHL Limited

- Blue Ribbon

- Batory Foods

- Diefenbaker Spice & Pulse

- Great Western Grain

- Best Cooking Pulses

Explore Convenience Food Industry Analysis: https://www.futuremarketinsights.com/industry-analysis/convinience-food

Explore Convenience Food Industry Analysis: https://www.futuremarketinsights.com/industry-analysis/convinience-food

Key Segments Covered by Chickpea Flour Industry Survey Report

By Product Type:

- Desi

- Kabuli

By Distribution Channel:

- Food Chain Services

- Modern Trade

- Convenience Store

- Departmental Store

- Online Store

- Other Distribution Channel

By End Use Application:

- Food & Beverage Processing

- Bakery or Baked Goods

- Confectionery and Desserts

- Savory Snacks

- Ready to Eat Products

- Pasta & Macaroni

- Energy & Protein Bars

- Meat Alternatives

- Dairy Replacements and Products

- Mayonnaise, Sauces, Condiments, and Dressings

- Extruded products

- Other Food & Beverages (Batter Mixes, Gravy Thickeners, Infant Nutrition)

- Retail Sales

- Supermarkets or Hypermarkets

- Departmental Stores

- Wholesale Stores

- Specialty Food Stores

- Other Stores

- Ready-to-Drink Beverages

- Dairy based Beverages

- Non-dairy or Plant-based Beverages

- Nutraceuticals

- Sports Nutrition

- Animal Feed

- Pet Food

By Product Claim:

- Organic or Non-GMO

- Conventional

By Region:

- North America

- Latin America

- Europe

- East Asia

- South Asia and Pacific

- Middle East and Africa (MEA)