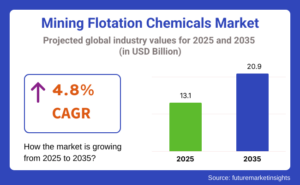

The global mining flotation chemicals market is projected to grow from USD 13.1 billion in 2025 to USD 20.9 billion by 2035, registering a CAGR of 4.8% over the forecast period. This growth is fueled by expanding extraction activities for copper, gold, and battery metals, where declining ore grades are prompting mineral processors to increase reagent dosages and adopt more selective chemistries. Among the various reagent types, collectors lead the market, holding the largest share of spending and are anticipated to grow at a faster CAGR of 5.9% through 2035 due to their critical role in enhancing mineral separation efficiency.

Track Evolving Market Trends: Request Your Sample Report! https://www.futuremarketinsights.com/reports/sample/rep-gb-184

Driving Forces Behind Market Growth

- Surge in Global Mining Activities:

Rapid industrialization and urbanization, especially in Asia and Africa, are driving increased demand for metals like copper, gold, zinc, and lithium, which rely heavily on flotation chemicals for efficient extraction. - Declining Ore Grades:

As high-grade ore reserves are depleting, mining companies are turning to lower-grade ores, which require more complex and intensive flotation processes, thereby increasing the consumption of flotation reagents. - Technological Advancements in Mineral Processing:

Innovative flotation chemistries and reagent formulations are enhancing metal recovery rates, improving selectivity, and reducing operational costs. - Sustainability Pressures:

The industry is witnessing a shift toward eco-friendly and biodegradable flotation chemicals to comply with environmental regulations and reduce the ecological footprint of mining activities. - Rise in Demand for Lithium and Rare Earth Elements (REEs):

The clean energy transition and electric vehicle boom are boosting the demand for lithium and REEs, which are processed using specialized flotation chemicals.

Market Challenges & Strategic Responses

Challenges:

- Stringent Environmental Regulations:

Growing environmental scrutiny around chemical use in mining processes is forcing companies to reformulate products and invest in greener alternatives. - Volatility in Raw Material Prices:

Fluctuations in raw material costs used in chemical production impact the pricing and supply of flotation reagents. - Water Scarcity and Wastewater Management Issues:

High water consumption and the need for responsible effluent disposal challenge flotation chemical usage, especially in arid mining regions. - Complex Ore Bodies:

Increasingly complex and polymetallic ore structures require more sophisticated and selective chemical reagents, increasing R&D costs.

Strategic Responses:

- R&D in Sustainable Chemicals:

Companies are focusing on developing bio-based and non-toxic flotation agents to meet regulatory standards and reduce environmental impact. - Strategic Collaborations and Acquisitions:

Market players are engaging in strategic partnerships with mining firms and acquiring niche chemical producers to diversify product portfolios. - Focus on Customization:

Reagent producers are offering tailored chemical solutions based on specific ore types and local processing conditions to enhance recovery efficiency.

Increased Market Demand: Get In-Depth Analysis and Insights with Our Complete Report! https://www.futuremarketinsights.com/reports/global-mining-flotation-chemicals-market

Regional Market Outlook

Asia Pacific:

The largest and fastest-growing regional market, driven by mining activities in China, Australia, and India. The region’s demand is supported by extensive mineral reserves, government-backed mining investments, and growing metal consumption across infrastructure and manufacturing sectors.

North America:

Home to well-established mining industries in the U.S. and Canada, North America is focusing on technological innovation and sustainability. Increased demand for copper, gold, and battery metals supports steady chemical usage in flotation.

Latin America:

Countries like Chile, Peru, and Brazil are witnessing significant growth due to their dominant copper and iron ore mining sectors. Supportive government policies and foreign investments further bolster market development.

Europe:

Europe’s market is shaped by a strong push for sustainable and environmentally compliant mining practices. Demand is particularly high for rare earth elements required for the region’s clean energy goals.

Middle East & Africa:

Emerging mining hotspots in South Africa, Ghana, and the Democratic Republic of Congo (DRC) are driving regional demand. Infrastructure development and resource exploration projects are spurring market opportunities.

Share Forecast Outlook

- Collectors remain the largest product segment, accounting for a significant market share, followed by frothers, flocculants, activators, and depressants.

- The metal mining segment, particularly copper, gold, zinc, and lithium, dominates demand due to widespread flotation-based processing techniques.

- Asia Pacific continues to hold the highest market share, with increasing adoption of modern mining technologies and flotation practices.

Key Players

- Sasol Limited

- SNF Floerger

- Chevron Phillips Chemical Company

- Dow Chemical Company

- Kemira Oyj

- Nouryon

- ArrMaz (Arkema)

- Huntsman Corporation

- Cytec Industries Inc.

Industrial and Institutional Chemicals Industry Analysis: https://www.futuremarketinsights.com/industry-analysis/industrial-and-institutional-chemicals

Mining Flotation Chemicals Market Segmentation

By Ore Type:

On the basis of ore type, the industry is categorized into sulphide ore and non-sulphide ore.

By Chemical Type:

By chemical type, the industry is divided into collectors, frothers, dispersants, activators, depressants, flocculants, and others.

By Region:

By region, the industry is divided into North America, Latin America, Western Europe, Eastern Europe, South Asia and Pacific, East Asia, and the Middle East and Africa.