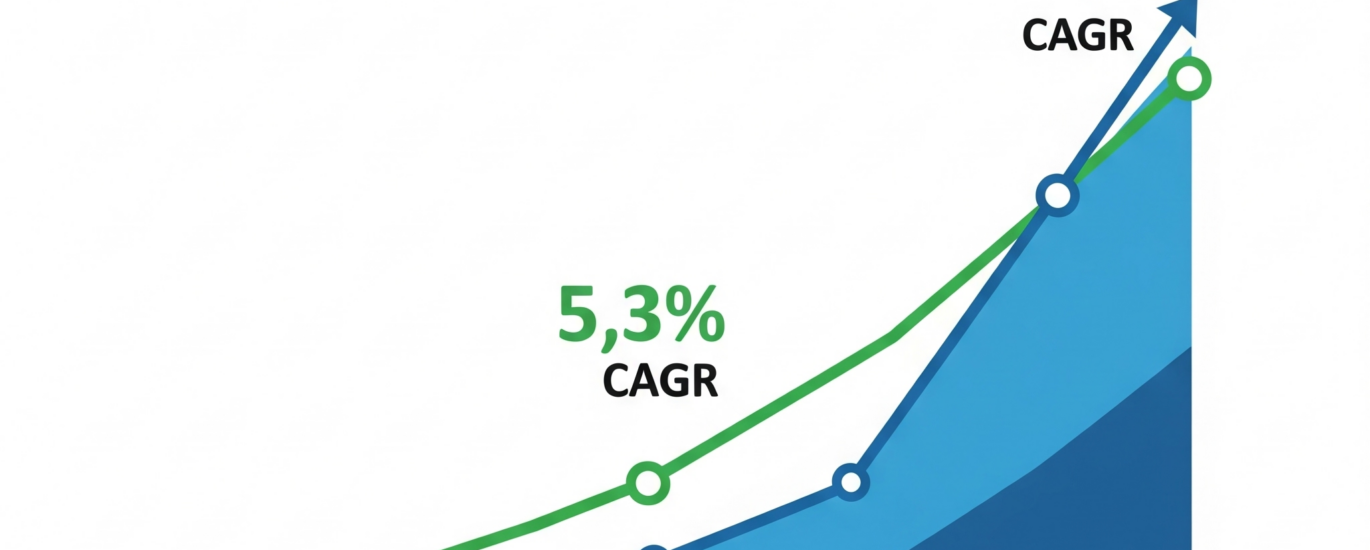

The automotive lead acid battery market is projected to expand from USD 31.26 billion in 2025 to USD 52.40 billion by 2035, registering a compound annual growth rate (CAGR) of 5.3% over the forecast period. The market’s growth is driven by the consistent need for dependable, cost-effective, and recyclable energy storage in vehicles—especially internal combustion engine (ICE) models, which continue to dominate global vehicle sales. Despite rising interest in electric vehicles, the versatility and affordability of lead acid batteries maintain their strong presence in starter, lighting, and ignition (SLI) applications.

Moreover, the widespread integration of advanced technologies in passenger and commercial vehicles requires stable power sources. The lead acid battery’s ability to deliver high surge currents, its mature recycling infrastructure, and its proven track record make it an essential component in the evolving automotive landscape. Developing regions with large vehicle fleets are increasingly investing in lead acid battery manufacturing to support local demand and reduce imports.

Get Ahead with Our Report: Request Your Sample Now!

https://www.futuremarketinsights.com/reports/sample/rep-gb-1482

Market Trends

-

Rising usage of enhanced flooded batteries (EFBs) and absorbed glass mat (AGM) batteries in advanced start-stop vehicles.

-

Increasing focus on battery recycling and closed-loop manufacturing systems.

-

Integration of intelligent battery sensors (IBS) to monitor battery health and performance.

-

Ongoing preference for low-cost and robust energy storage in developing economies.

Driving Forces Behind Market Growth

-

Continued dominance of ICE vehicles globally, requiring SLI batteries.

-

Widespread vehicle ownership in emerging markets, increasing demand for aftermarket battery replacements.

-

Growth of the commercial vehicle sector, including trucks and buses.

-

Demand for reliable backup power in electric and hybrid vehicles for safety and control systems.

-

Strong availability of recycling networks reducing environmental impact and supporting circular economy.

Challenges and Opportunities

-

Challenges:

-

Growing penetration of lithium-ion batteries in electric vehicles may limit growth in specific segments.

-

Environmental concerns over toxic lead content and disposal.

-

Weight and energy density limitations compared to newer battery chemistries.

-

-

Opportunities:

-

Increased focus on battery reconditioning and reuse to extend product lifecycle.

-

Innovation in sealed and maintenance-free lead acid batteries.

-

Growing aftermarket sales driven by extreme weather conditions and battery wear.

-

Strong demand from fleet operators and logistic companies seeking affordable battery options.

-

Recent Industry Developments

-

Clarios announced a new investment in AGM production facilities in 2024 to meet growing demand for start-stop systems.

-

Exide Technologies launched an extended-life lead acid battery line for commercial trucks and buses.

-

GS Yuasa expanded its partnership with European OEMs for lead acid battery supply.

-

East Penn Manufacturing introduced an advanced EFB product line optimized for fuel-saving technologies.

Thorough Market Evaluation: Full Report

https://www.futuremarketinsights.com/reports/automotive-lead-acid-battery-market

Regional Analysis

-

North America:

-

Strong aftermarket segment due to high vehicle ownership and extreme climate variations.

-

Key players expanding AGM battery production to meet demand for fuel-efficient systems.

-

-

Europe:

-

Shift toward eco-friendly battery technologies aligning with strict emissions regulations.

-

High uptake of start-stop vehicles supporting AGM and EFB lead acid battery sales.

-

-

Asia-Pacific:

-

Largest market due to high vehicle production in China, India, and Japan.

-

Strong government incentives for battery recycling and manufacturing.

-

-

Latin America and Middle East & Africa:

-

Growing demand from the used car market and commercial fleets.

-

Investments in local production to reduce reliance on imports.

-